The debate over electric cars has been—and continues to be—framed as an ideological battle. On one side are those who see them as the only viable path to decarbonizing transportation; on the other are those who point to their costs, infrastructure limitations, and industrial challenges. Then the data comes along and brings the discussion back to the most useful ground: that of facts.

Figures releasedby the European Environment Agency (EEA) show that in 2025 , the average emissions from new cars registered in the European Union, along with Norway and Iceland, fell to 96.7 grams of CO₂ per kilometer, compared to the 106.7 grams recorded in 2024. This represents a reduction of about 9% in just one year, achieved without a significant contraction in the market, which remained essentially stable at 10.8 million new registrations.

This result is primarily driven by the growth of battery-electric vehicles. In 2025, their share reached 18.9% of the European market, up from 14.4% the previous year. Plug-in hybrids are also on the rise, increasing from 7.1% to 9.7%.

When Policies Work

One thing stands out from these figures: emissions decrease as registrations of zero-emission vehicles increase. This may seem like an obvious observation, but it takes on particular significance at a time when the automotive industry continues to call for greater flexibility regarding climate targets.

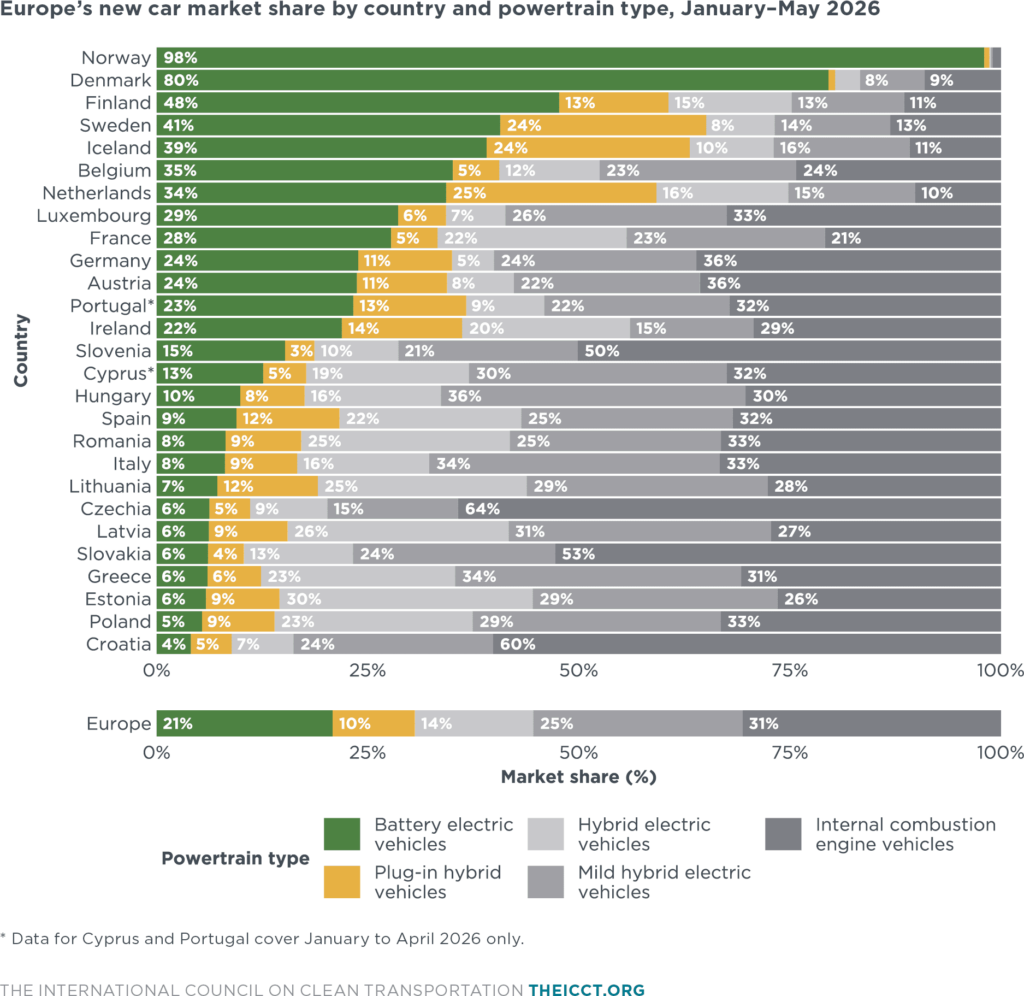

The EEA explicitly attributes the decline in emissions to the increase in the share of electric vehicles among new registrations. This is also confirmed bythe International Council on Clean Transportation (ICCT), which reports that between January and May 2026, electric cars accounted for 21% of new registrations in Europe—five percentage points more than during the same period the previous year. During the same period, cars with traditional internal combustion engines fell to 31% of the market, losing nine percentage points. This is a structural trend that is changing the composition of the market.

A Two-Speed Europe

But the transition is not proceeding at the same pace everywhere. Norway continues to be a nearly unique case: in 2025, 96% of newly registered cars were fully electric. Denmark and Iceland follow, with shares of 69% and 43%, respectively. Looking at the first few months of 2026, the gap remains evident. In Germany, electric cars accounted for 24% of the market; in France, 28%; while in Italy, they stood at 8%, and in Spain, 9%.

The data from Italy reveals a vulnerability that goes beyond consumer preferences: sporadic incentives, unevenly distributed charging infrastructure, and one of the oldest vehicle fleets in Europe continue to slow down the technological transition. While Northern Europe is discussing how to manage the now-massive adoption of electric vehicles, in Italy the main issue remains accessibility.

Corporate Fleets as a Key Lever

One of the least-discussed aspects concerns the role of businesses. According to the ICCT, approximately 60% of new vehicle registrations in Europe are attributable to corporate fleets. This is where a significant part of the climate challenge is played out, because corporate vehicles travel more kilometers on average and are replaced more quickly, subsequently fueling the used-car market. The results show that this approach can work. In France, for example, large companies have achieved such a high share of electric vehicles that they will already exceed the European Commission’s 2030 targets by 2026.

Italy, on the other hand, still appears to be lagging behind: electric vehicles make up only about 5% of company fleets, which is far from the targets Brussels has set for the coming decade.

The risks

Data from 2025 and the first few months of 2026 show that the reduction in emissions from light-duty vehicles is not a theoretical possibility but a process already underway; however, this does not mean the goal has been achieved.

The ICCT notes that, in the absence of stringent interim targets, some manufacturers have historically tended to slow down their efforts once they have met their targets, only to call for regulatory action as subsequent deadlines approach.

Climate policies work when they remain predictable and consistent over time. The European automotive industry is proving its ability to adapt to emissions reduction targets; the market is responding, and emissions are actually declining. We can only hope that this transformation, which is finally beginning to yield measurable results, will not be hindered.